The SA economy is expected to have contracted by 30.6% for the second quarter of the year, when lokdown was in full-force.

- B4SA, which represents a majority of SA businesses partnering in their response to Covid-19, has released a 12-point plan it says will accelerate economic recovery.

- It says the plan, together with policy interventions, could increase GDP by R1 trillion, create up to 1.5 million jobs, and increase tax revenues by R1 billion per year.

- But it says its plan will require about R3.4 trillion in funds over the next three years.

South Africa is at a fork in the road and can either stick to the status quo and risk reversing the socio-economic gains made since 1994, or leadership can take the difficult, even “unpalatable” decisions needed to drive investment and inclusive growth, says Business For South Africa.

The organisation, which represents a majority of South African businesses partnering in their response to the Covid-19 pandemic and the economic shock it caused, on Friday released a 12-point plan that it says will accelerate the country’s economic recovery.

B4SA says the plan, in conjunction with policy interventions, could increase GDP by R1 trillion, create up to 1.5 million jobs and and increase tax revenues by R100 billion per annum.

Some of the interventions include securing affordable electricity supply, fast tracking the green economy, expanding ports and accelerating e-commerce.

B4SA estimates its economic recovery plan will require R3.4 trillion in funds over the next three years. This would push public sector debt from R4 trillion to R6.4 trillion. The estimate does not take into account the potential rescue funds for corporates or unforeseen bailout for state-owned enterprises.

“This funding need cannot be met by domestic sources, nor is it possible for the South African reserve Bank to address the shortfall in a responsible and sustainable manner through monetary measures,” a document from B4SA reads.

The private sector could step in to help fund economic infrastructure, which would result in “faster and more sustainable” economic growth, it said. This would relieve pressure on state coffers.

B4SA said that about $10 trillion of capital is available from international markets, including Sovereign Wealth Funds and Development Finance Institutions, among others. SA could successfully compete for this funding by securing investor confidence, for example by improving ease of doing business.

The SA economy was already in recession once the Covid-19 pandemic struck and a lockdown was instituted in late March. The county’s GDP is expected to contract anywhere between a record 7% and 13% this year, leading to higher unemployment and a plunge in tax revenues.

This will have dire consequences for public debt, with Treasury projecting a budget deficit of 14.6%, slightly higher than B4SA’s estimate of 13.3%.

“In the absence of growth enhancing structural reforms, budget deficits are expected to remain high and government debt is expected to exceed 100% of GDP in 2023,” B4SA said in a statement on Friday morning.

For the second quarter of the year, which covers the months of April, May and June, B4SA projects a GDP contraction of 30.6% due to the economic impact of the lockdown, which was in full force in April.

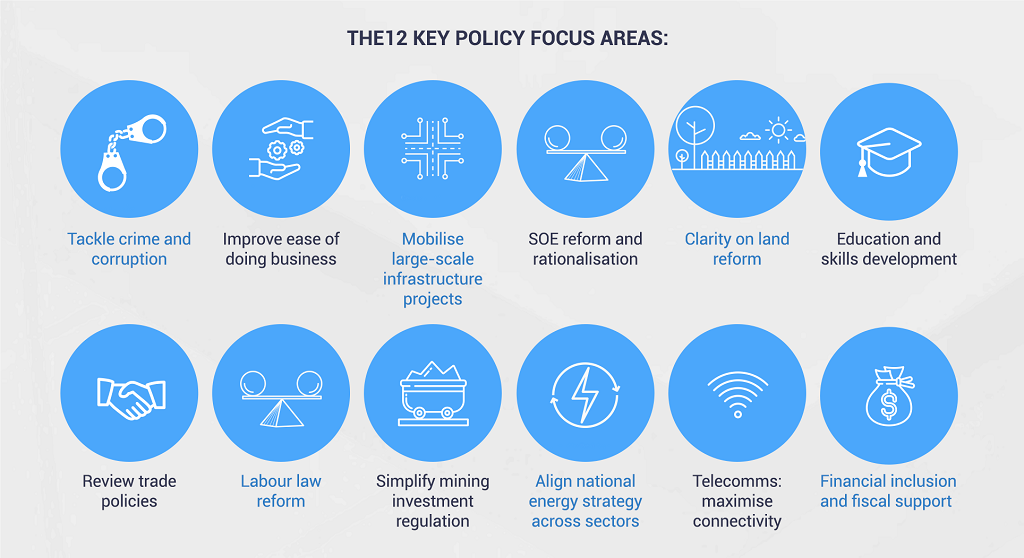

In addition to 12 key initiatives that must be undertaken, B4SA has identified 12 policy focus areas that need to be addressed.

The group is hold a media briefing at 10:00 to further unpack its plan.

{kind=link}